As an incorporated professional, insurance should be a key part of your financial plan. Most of us think of insurance as a means to protect ourselves during our working years or to provide for our loved ones after we’re gone. While this is true, insurance can offer so much more. It can protect your income, safeguard your practice, and enhance your retirement savings.

In this article, we’ll explain how proper insurance planning can fit into your overall financial plan.

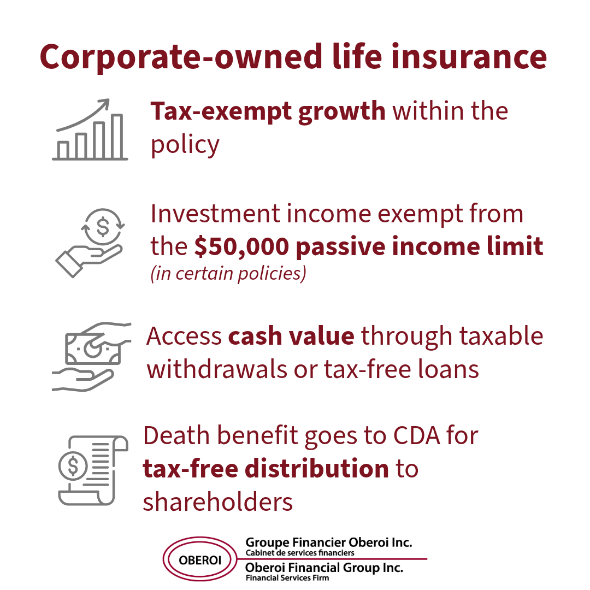

Corporate-owned life insurance: Your “no-limit corporate TFSA”

Let’s begin with corporate-owned life insurance. This is where your corporation is the policy owner and beneficiary of a permanent life insurance policy, and you as the business owner (or another key person) are the insured.

Although corporations can’t have a tax-free savings account (TFSA), corporate-owned life insurance can offer similar features and benefits. Namely, that you can use it to grow and withdraw your money, potentially tax-free. Here are some of the advantages of corporate-owned life insurance:

- Money that grows within the policy is tax-sheltered.

- Investment income in certain policies is exempt from the federal $50,000 passive income limit that could reduce your company’s access to the small business deduction.

- You can access the cash value of the policy through taxable withdrawals. You may also be able to access the cash value through tax-free third-party loans, where your corporation may be able to borrow from banks or other third-party lenders using the policy’s cash value as collateral.

- When you (or the key person insured by the policy) die, a tax-free death benefit goes to your Capital Dividend Account (CDA). From there, your company can pay tax-free distributions to shareholders.

Corporate-owned life insurance is a flexible tool that helps you invest and grow your money in a tax-sheltered way, all while offering an extra layer of financial protection.

Disability and critical illness insurance: Protect your earnings

For self-employed incorporated professionals, your income is directly tied to your ability to work. In the event of an illness or injury, disability insurance can help protect you and your family. This coverage replaces your income if you’re unable to work for an extended period of time. Disability insurance should typically be owned personally – not through your corporation – and is an important part of your risk management plan.

Meanwhile, corporately held critical illness insurance gives your corporation a tax-free, lump-sum payment if you are diagnosed with one of the covered illnesses. The most common covered illnesses are life-threatening cancer, heart attack, or stroke. The payout can help you cover medical costs and maintain financial stability as you navigate through your illness and recovery. With added benefits such as the return of premium rider, critical illness insurance almost becomes a must.

Disability and critical illness insurance give you and your loved ones a safety net to fall back on when life throws you a curveball.

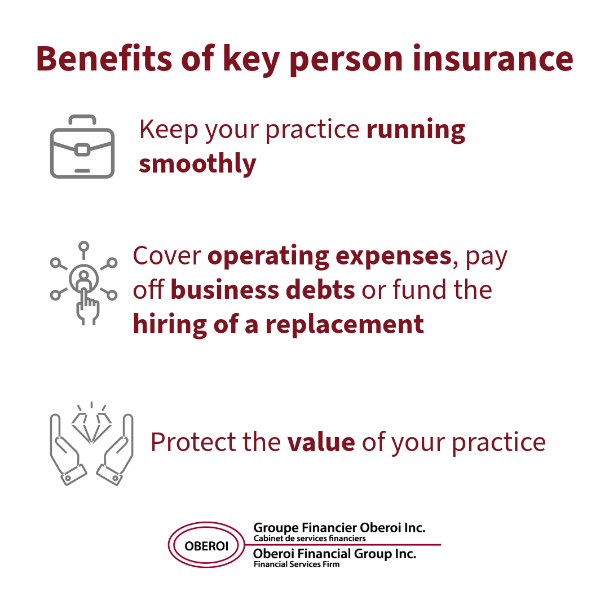

Key person insurance: Safeguarding your practice

As an incorporated professional, your practice is often built around your expertise. Whether you run a medical practice, law firm, or dental clinic, your business relies on you. This is where key person insurance comes in. Key person insurance is critical illness or life insurance that your corporation purchases on your life. If you get sick, or when you die, the benefit can help keep your practice running smoothly. It can cover operating expenses, pay off business debts, or fund the hiring of a suitable replacement. This is vital for maintaining business continuity and protecting the value of your practice.

For many professionals, key person insurance is also part of a larger business succession plan. It ensures that your business doesn’t suffer financial disruption in the event of an unexpected loss. This is especially important if you plan to sell your practice or pass it on to others.

Life insurance for retirement savings: Enhancing your wealth

Permanent life insurance policies – like whole life or universal life insurance – offer more than just a death benefit. They also build cash value, which grows over time and can become a valuable part of your retirement plan. The advantage of this growth is that it’s tax-deferred. This means you won’t pay taxes on the accumulation unless you decide to withdraw the cash value from the policy directly. Using third-party collateral loans may even eliminate the tax burden of such withdrawals, but it’s important to consult with your tax advisor. They can help you understand the tax considerations before you take action.

Your permanent life insurance policy can also serve as a savings vehicle for retirement, complementing other strategies like RRSPs or pensions. The death benefit can support your estate planning, providing your family or beneficiaries with a tax-free payout when the time comes. By using life insurance as part of your retirement strategy, you create a flexible, tax-efficient asset that can grow alongside your other retirement savings. It’s a way to hedge against the risks of other market-dependent investments, offering stability and tax advantages.

Bringing it all together: Insurance as a financial tool for you and your business

Incorporating insurance into your financial plan offers several benefits: protecting your income, securing the future of your practice, and enhancing your retirement savings.

If you’d like to learn more about how insurance fits into your financial plan, reach out! We’re here to simplify the process and help you make the best choices for your family, your practice, and your future.